cdbsmith

- 6

- 0

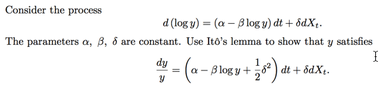

cdbsmith said:I am new to SDE, and especially Ito's Lemma. I have a question that I simply cannot answer. It attached.

Can someone please help?

Euge said:Hi cdbsmith,

Let $u = \log y $, $\mu_t = \alpha - \beta u$, and $\sigma_t = \delta$. Then $du = \mu_t dt + \sigma_t dX_t$. Let $g(u) = e^u$. We have by Ito's lemma

$\displaystyle dg = \left(g'(u)\mu_t + \frac{g"(u)}{2}\sigma_t^2\right) dt + g'(u)\sigma_t\, dX_t $,

$\displaystyle dg = \left[e^u(\alpha -\beta u) + \frac{e^u}{2}\delta^2\right] dt + e^u\delta\, dX_t$,

$\displaystyle \frac{d(e^u)}{e^u} =(\alpha - \beta u + \frac{1}{2}\delta^2) dt + \delta\, dX_t$,

$\displaystyle \frac{dy}{y} = (\alpha - \beta\log y + \frac{1}{2}\delta^2) dt + \delta\, dX_t$.

cdbsmith said:Thanks, Euge!

But, can you explain to me the steps? Ito's Lemma is confusing for me and I'm having a hard time understanding it.

Thanks again!